..

The dollar is dead, long live the dollar

April 05, 2023

Every now and then, a story about some country seeking to diversify away from the US dollar kicks off a frenzy about the inevitable collapse of dollar dominance. Lately, there’s been more than a few such headlines, including:

- Russia embracing the Chinese yuan for much of its global trade

- Saudi Arabia considering invoicing oil exports to China in yuan

- France buying gas from China in yuan

- Brazil and China agreeing to ditch the dollar for bilateral trade

- BRICS countries planning to develop a new reserve currency

- Kenya promising to ditch the dollar for oil purchases

- ASEAN members discussing dropping the dollar for cross-border payments

- India settling some trade in rupees

Naturally, these have provided a fertile ground for gold bugs, crypto shills, hyperinflation truthers, techno-libertarians, anti-imperialists (read: anti-US zealots), and run-of-the-mill grifters to stoke fear about the dollar’s imminent death and its supposedly catastrophic consequences for the United States and the global economy.

But even mainstream media outlets and smart, well-meaning analysts have gotten swept into the current wave of hysteria.

.

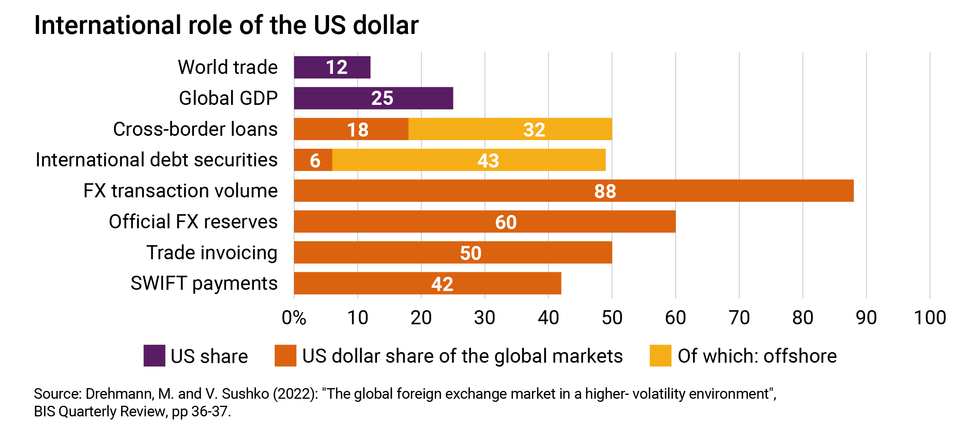

Yet rumors of the dollar’s death are greatly exaggerated. Going by most usage measures, the dollar remains incontrovertibly dominant in global trade and finance, if a little less so than at its apex.

Whereas most currencies are only used domestically or in cross-border transactions that directly involve the currency’s issuer, the dollar continues to be widely used for funding, pricing, trade invoicing and settlement, and cross-border borrowing and lending even when the US is not involved.

.

Even China, in an environment of intensifying geopolitical competition with the US and having just witnessed Washington’s weaponization of the dollar against Russia, has had no choice but to continue accumulating dollar-denominated assets.

.

The Chinese yuan, meanwhile, is not a viable alternative because of Beijing’s authoritarian and statist bent. In fact, Xi Jinping’s policy preferences – economic self-reliance, financial stability, common prosperity, and political control of the economy – run directly counter to his global-currency ambitions.

Despite its growing role in the global economy and long-standing desire to unseat the dollar, China lacks the investor protections, institutional quality, and capital market openness required to internationalize a yuan that is still not fully convertible overseas. Persistent currency and capital controls, an opaque banking system with too many non-performing loans, spotty contract enforcement, and often arbitrary and draconian regulations will all continue to undermine Beijing’s efforts to elevate the yuan.

.

The most serious threat to dollar dominance might come not from abroad (Europe, China) or from beyond (cyberspace) but from within. The United States is still the most powerful nation on earth, but it’s also the most politically divided and dysfunctional of all the major industrial democracies. The single biggest risk to the dollar’s global status is that growing inequality, tribalism, polarization, and gridlock eventually undermine trust in America’s stability and credibility.

At the end of the day, though, no matter how much the dollar seems to lose its shine, global currency status is about relative – not absolute – advantages. Without a viable challenger, it’s very unlikely that the dollar will lose its special role anytime soon – for better or worse. You can’t replace something with nothing.

https://www.gzeromedia.com/by-ian-bremmer/the-dollar-is-dead-long-live-the-dollar

..